In 2000, many of us watched the movie, "The Perfect Storm." The blockbuster showed us how a number of meteorological factors converged to form the perfect storm. Within the insurance industry, there has been a confluence of key factors that led to a "perfect storm" that began in 2001 and still continues. We've seen an unprecedented catastrophe on Sept. 11, 2001; investment results that have declined in stocks and bonds for a three-year period, which hasn't happened since 1939-41; years of price decreases while inflation significantly has risen; and reserve deficiencies that partially are attributable to the increase in jury awards.

To understand the insurance industry, you must understand that businesses have mutually beneficial relationships with their commercial insurance carriers. Insurance allows customers to transfer certain business risks for a premium charge in exchange for achieving financial protection. For large organizations, insurance becomes more of a financial transaction where the insurer only responds when losses exceed an agreed-upon level, or self-insured retention.

One difficulty with understanding insurance often involves how carriers extend coverage and determine premiums. As a roofing contractor, you probably find it difficult to understand why you pay so much for insurance premiums, often for many years before experiencing a significant claim. And you may assume a commercial general liability (CGL) policy will provide coverage for most, if not all, liabilities you may face. However, it is the policy language that determines what is covered when a claim is made.

An insurance policy is a contract between you and an insurer that specifies terms and conditions to which each party must adhere. I will attempt to demystify the insurance purchasing process by discussing the dynamics of the industry, pricing and coverage.

Insurance industry economics

The insurance industry is heading into the third year of a "hard market," meaning pricing trends exceed the increase in claim-cost trends. To understand the current state of the insurance industry, consider what happened leading up to 2003.

During the 1990s, commercial lending institutions were averaging a 15 percent return on equity while the property and casualty insurance industry averaged only a 6 percent to 7 percent return on equity. From 1997-2001, the average return on equity for the property and casualty industry declined every year. The major commercial insurance lines—automobile, workers' compensation, package, general liability and property—lagged well behind Fortune 500 companies' historical 13 percent to 14 percent returns on equity.

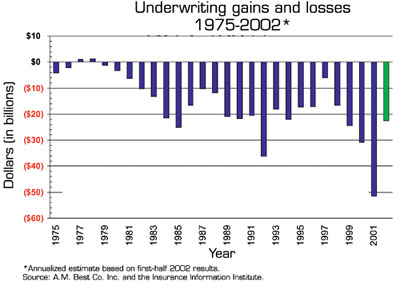

The property and casualty industry's combined ratio averaged 108 percent in the 1990s and climbed to 110 percent in 2000 and 115.7 percent in 2001. The combined ratio represents losses (paid and reserved) plus expenses as a percentage of premiums collected. Therefore, in 2001, the industry paid out $115.70 for every $100 it took in.

Every year since 1979, the property and casualty industry has produced an underwriting loss—a combined ratio of more than 100 percent. That loss was $31 billion in 2000 and $52 billion in 2001 and is forecasted by the Insurance Information Institute, New York, and A.M. Best Co. Inc., Oldwick, N.J., to be $22 billion in 2002.

Property and casualty insurers paid $52 billion more in claims and expenses than they collected in premiums in 2001.

The property and casualty industry has been able to survive despite not making an operating profit since 1978 because of net investment income.

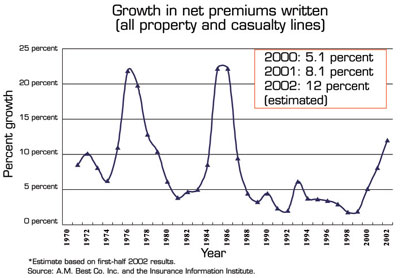

Actual and estimated growth in net premiums

The net investment income for the industry has increased almost every year since 1975 and peaked at $41.5 billion in 1997. Net investment income for the property and casualty industry in 2001 was $37 billion compared with an underwriting loss of $52 billion. This is significant because for the first time in the insurance industry's history, it recorded an after-tax annual loss of $7 billion.

On average, the insurance industry invests 66 percent of its assets in bonds and 21 percent in common stock with the balance held in real estate, cash and other investments. During the past several years, operating profits continued to deteriorate and investment income declined because of historically low interest rates and three consecutive years of declining stock values. These trends are driving a renewed focus on improving operational efficiency and underwriting performance.

Industry reserving

Over this same three-year period, the insurance industry has seen an increase in reserving, or setting aside funds to pay for future claims, for current-year business and business from prior years.

Reserving is approached in two contexts. The first is when a claim occurs. A claim handler collects pertinent information about the claim and relies on claim payment history for similar claim types in a given jurisdiction. Armed with that information, the claims handler makes an informed estimate of the ultimate payout for that particular claim. That information is entered into the insurance company's system as the reserve for the particular claim.

Insurers know many claims' events already have occurred that will take years to be reported. These claims are accounted for in a category called incurred but not reported (IBNR). Actuaries look at historical data and calculate IBNR events for a given line of insurance. This is translated into a "loss-development factor" that then is multiplied by the incurred loss ratio for that line of business to arrive at the ultimate loss ratio for a line of coverage in a given year.

During the past 10 years, it has been necessary to increase prior-year loss reserves beyond what the insurance industry had predicted when the reserves first were established. Coupled with ongoing weak investment performances, it has been difficult for insurance companies to allocate the necessary capital to fund their loss reserves.

Several industry-rating agencies estimate the property and casualty industry significantly underreserved for asbestos and environmental claims. In addition, increases in jury awards and claim-cost inflation, particularly medical costs, have put additional strains on the industry's reserves. New York-based Morgan Stanley estimates the total reserve underfunding for the insurance industry is $120 billion.

Rates and pricing

Many property and casualty insurers use the Insurance Service Office (ISO) and National Council on Compensatory Insurance (NCCI) for rate-making purposes. These agencies receive information about premiums and losses by class code, state and territory to establish loss-cost figures.

Loss costs usually are based on average losses during a prior four-year period. ISO and NCCI may exclude or discount years that substantially are higher or lower than the average so they do not cause wide variability in loss costs. These figures then are submitted to each state's department of insurance that must approve all or a portion of the indicated loss-cost increase or decrease. Individual insurance companies then file loss-cost "multipliers," expense factors for each company, that are multiplied by the loss costs for each business line to determine rates.

There are several weaknesses in this process. The first is a state may not approve the entire rate increase. Second, the rate-making process uses a rearview-mirror approach—it may not fully recognize emerging claims issues or risk exposures caused by claims that are not reported until years after they occur, such as construction-defect and asbestos claims. In addition, the process may be slow to recognize cost inflation or other significant factors.

There are several other factors by which rates are multiplied to determine the price for a particular policy, such as increase limits factors (based on the limits desired), experience modifiers, company deviations, and discretionary credits or debits. Many insurance companies have a number of subsidiary underwriting companies with which they write policies for different business types. Based on certain guidelines, a policy for an insured is placed in one of the insurer's underwriting companies, which may affect the insured's premium.

Discretionary pricing comes into play based on the loss trends of the business seeking insurance, predictability of its loss frequency, funding needed for severe and catastrophic losses,key trends within the state where it operates, and quality of its management and loss-control programs.

This brings us to the trends that have emerged during the past several years and some reasons why you may have experienced significant rate increases for new and renewal policies.

On average, premium rates decreased for the property and casualty insurance industry every year from 1994-99. Rates began to increase in 2000, but the increase did not keep pace with the annual inflation in claim costs. Annual premium rate increases began to exceed annual claim cost increases in 2001. It is estimated by the Insurance Information Institute that the average property and casualty rates charged in 2002 merely will match rates charged in 1995-96.

The cost for businesses to transfer property and casualty risks decreased 42 percent between 1992-2000 and increased 15 percent in 2001. The Risk Insurance Management Service's Benchmark Survey and Insurance Information Institute estimate that this cost increased 30 percent in 2002. Even with these increases, the cost of transferring risk to insurers is substantially less than it was a decade ago.

Litigation trends and coverage

Although the cost of insurance decreased for most of the 1990s, the expenses associated with defending against and settling legal claims significantly increased and continue to do so.

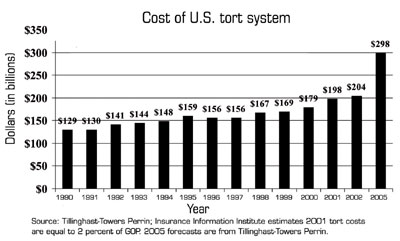

The cost of the U.S. tort system has consumed 2 percent of the gross domestic product (GDP), on average, since 1990. Current trends would bring this to 2.4 percent of GDP by 2005, according to a study by Tillinghast-Towers Perrin, Weatogue, Conn. Tort costs for commercial insurance lines were $22 billion in 1980 and $85.4 billion in 2000. Unfortunately, the U.S. tort system is extremely inefficient with only 20 percent of payments compensating victims for their economic losses.

Tort costs annually consumed 2 percent of gross domestic product (GDP) on average since 1990 and are expected to rise to 2.4 percent of GDP by 2005. Tort costs equaled $636 per person in 2000 and are expected to rise to $1,000 per person by 2005.

The longest-running mass litigation in U.S. history is asbestos-related. Many in the insurance industry believed asbestos-related claims were winding down in 1999.

To the contrary, a claims resurgence occurred during the past several years. Several fundamental shifts have occurred during this recent surge in litigation. Plaintiffs' lawyers have moved their focus from major manufacturers to suppliers, distributors, building and facility owners, and contractors ranging across 75 industry types. Claims that once were filed by plaintiffs who clearly had developed asbestos-related illnesses, most notably mesothelioma, now are being filed by plaintiffs who have no signs of illness or injury. Another major dynamic is that numerous targeted defendants have filed for bankruptcy protection.

In 2002, the RAND Institute for Civil Justice, Santa Monica, Calif., completed a comprehensive study, "Asbestos Litigation Costs and Compensation," about asbestos litigation. The study included cases through the year 2000. Some of its key findings follow:

What's of even greater concern is that the RAND Institute for Civil Justice study predicts that 500,000 to 2.4 million more claims could be filed. In addition, 65 percent of compensation has been awarded to claimants with no malignant injuries, and legal and other transactional costs consumed more than half of total spending.

The RAND Institute for Civil Justice study estimates the eventual total cost of asbestos claims could be $200 billion to $265 billion. Fifty-four billion dollars already has been spent on asbestos litigation and settlements through the end of 2000. In addition, pollution coverage claims continue to come under the scrutiny and interpretation of state courts, producing mixed outcomes.

Mold is the next major type of mass litigation emerging in the United States. In 2000, mold was not a significant claims concern for most major commercial insurers. Now, mold has resulted in about $3 billion in incurred commercial claims.

Unlike other mass litigation, mold litigation is not concentrated in a few states. The current focus in the commercial arena is on buildings where there are a sufficient number of litigants and defendants to make a case economically feasible. Frequently targeted properties include schools, government buildings and apartment buildings. Defendants include building owners, especially those of publicly owned buildings; property owners, especially those of apartment buildings; general contractors and developers; architects and engineers; building material manufacturers and suppliers; and specialty contractors, such as roofing and heating, ventilating and air-conditioning contractors.

Because the frequency, severity and ultimate exposure of mold claims are not known, many insurers exclude or limit coverage for such claims. These exclusions take various forms, and new approaches are being introduced.

Construction-defect claims, which began in the early 1980s in southern California, are an ongoing concern to the insurance industry. The economic incentive for plaintiffs' lawyers is similar regardless of the state—multiple defendants allege multiple defects. The primary context where this type of quasi class-action suit is found is in new residential construction of tract housing, condominiums or multifamily developments. The risk of construction-defect litigation greatly increases with the convergence of the following primary drivers:

The states currently with the most construction-defect litigation are Arizona, California, Colorado, Nevada, Oregon, Texas and Washington.

Exterior insulation and finishing systems (EIFSs) also have produced property damage claims that negatively have affected manufacturers and contractors for several years. The problem is once water enters an EIFS, it does not have a way to escape, resulting in degradation of wood and similar building materials. Some EIFS claims also now include claims of bodily injury because of mold. States seeing a majority of these claims are Alabama, California, Florida, Georgia, Louisiana, New Jersey, North Carolina, Oregon, South Carolina and Washington.

In addition, risk-transfer losses caused by contractual or additional-insured claims significantly have increased during the past several years because of broadening CGL policy language and case-law interpretation. Insurers have begun to tighten coverage language and charge for these emerging exposures, which largely were provided at little to no premium in the past.

There also are unique risk-transfer issues in Illinois and New York. New York has a labor-law statute that imposes a strict liability standard for fall losses on a construction project to the owner or general contractor unless liability has been contractually assumed by a subcontractor. In addition, these losses tend to be quite large, and, therefore, it is difficult from an insurer's perspective to spread risk and obtain an appropriate price for this exposure. It is becoming more difficult for contractors who have a fall exposure, such as roofing contractors, to obtain general liability coverage in New York.

The Illinois situation is somewhat different. The Illinois Supreme Court, in its decision for John Burns Construction Co. v. Indiana Insurance Co., provided for a general contractor to target a subcontractor, who may be required to pay for the damages of all subcontractors, and take its policy off the table for coverage consideration. This has made subcontractors responsible for paying entire claims where contributions were allowed in the past. This has increased costs for subcontractors who previously were minimally involved in a claim if at all.

As prices fell during the soft market of the 1990s, insurance policy terms and conditions significantly were broadened. That trend has reversed, and now there is a tightening of optional coverage offerings. In addition, because of the litigation dynamic, more insurers are providing exclusion endorsements or coverage limitations for EIFS; subsidence, or land movement; mold; and residential construction.

Terrorism legislation

Sept. 11, 2001, saw the advent of the world's largest insured catastrophic loss, estimated at $40 billion. The next closest single event insured loss was Hurricane Andrew in 1992 at $19.6 billion. The Sept. 11, 2001, events also created the first-ever workers' compensation and life insurance catastrophes—estimated at $2 billion and $2.7 billion, respectively, according to the Insurance Information Institute.

Before Sept. 11, 2001, the property and casualty industry had less than $300 billion in policyholder surplus. This policyholder surplus was split fairly evenly between commercial and personal property and casualty lines. The surplus held in property and casualty commercial insurance lines following the Sept. 11, 2001, attacks was reduced by nearly one-third. To lose one-third of the industry's surplus in one day is a major concern.

That concern gave rise to coverage availability issues for terrorist act—especially for properties and projects viewed as high risk. Many insurers are measuring their risk accumulation (aggregation) to determine how many properties and workers they insure in a given area and how much aggregate loss they may assume in one catastrophic event. Risk aggregation is a relatively new concept for workers' compensation and group life insurers and, to a lesser extent, automobile and general liability lines. Property insurers have had aggregation models for years for events such as hurricanes, earthquakes, wind, floods and other natural disasters.

Restrictions on terrorism coverage availability negatively affected the economy as lenders became less willing to fund high-profile projects or properties that did not have this coverage.

One of the basic tenets of insurance is the pooling of risks—using the premium of many to pay for the losses of a few. This principle breaks down when a single event simultaneously affects many lines of coverage and insureds. Another industry tenet is the ability to accurately assess risk and price for exposure. Frequency and severity of potential claims must be stable to be estimated.

Because these two basic tenets are not met in terrorist acts, Congress and the insurance industry believe the best way to handle future terrorism risks is through federal terrorism support for private insurance companies.

President Bush recently signed the Terrorism Risk Insurance Act of 2002. As of early January, many details related to implementation of this act still needed to be determined by the U.S. Treasury Department, but the act has many important elements (see "Terrorism—a new insurance threat," for details).

Insurers have informed customers about the new federal act and that exclusions on their policies related to the definition of an "act of terrorism" will be suspended during which time insureds have an opportunity to purchase coverage for terrorism. Insurers are making coverage available without terrorism exclusions and may provide other options, as well.

The future of the industry

Hartford, Conn.-based Conning, an insurance industry research company, predicts the property and casualty industry will have seen the increase in net written premiums peak in 2002. The company further predicts premium increases will continue in 2003 and 2004 but at lower growth rates than in 2002. Conning estimates the industry's combined ratio will improve from a projected 109 percent in 2002 to 105.2 percent in 2003 and 104.5 percent in 2004 barring unusual catastrophes. Despite these improvements, Conning estimates that after-tax income and return on equity for the property and casualty industry only will improve marginally during this period.

Improvements in overall results and return on equity will be slow because of numerous factors. Certainly, an economic recovery will have an effect, but at this point, it has been slow to emerge. As mentioned earlier, there still is a need for significant reserve strengthening by the insurance industry, as well as a need to find more effective ways than litigation to achieve conflict resolution. The historical data show that hard insurance markets typically last no more than three years. This fact coupled with the continued weakness in the investment markets means the insurance industry must continue to make fundamental enhancements in its underwriting processes and overall cost structure. This is necessary for insurers to achieve the combined ratios and return on equity needed to meet customers' needs while providing adequate returns to investors.

What you can do

You may continue to see premiums rise and terms and conditions tighten. Certain business industries in parts of the United States may have problems finding certain types of coverage.

As insurance companies move to more traditional underwriting models, there is much more emphasis on the quality of the customer. It is incumbent upon your business to implement best practices related to hiring, training, safety, quality-control, risk transfer and water-damage prevention programs. These practices must be supported by management and implemented throughout your organization. In addition, your business should have a successful loss-management program that includes an effective accident-investigation program, incentives for worker compliance and a practical injury-management program.

Effectively using a preferred provider organization and other cost-management programs can go a long way to mitigate claims' dollars paid. You should partner with insurers to implement the programs needed to effectively mitigate and manage losses. Insurers, as well as NRCA, have established many model programs that you can modify and implement.

National tort reform is needed to provide a more efficient means of getting appropriate settlements and having a higher portion of settlement dollars directly go to injured parties. Efforts to support tort reform at national and state levels will help restore predictability to the insurance buying process.

The hard insurance market still remains though it may have peaked. Expect to continue to see tightening coverage terms and conditions as insurers provide a more disciplined underwriting approach to the market. The current financial results of insurers indicate that pricing still is below appropriate levels. To get to required combined ratios, insurers will place greater emphasis on underwriting and pricing for exposures assumed. You must do your part to control and manage losses through effective implementation of risk-management programs.

Kathy Woodliff is director of general liability for Zurich North America, Schaumburg, Ill.

Terrorism—a new insurance threat

President Bush signing the Terrorism Risk Insurance Act of 2002 was a major step to help the insurance industry respond to terrorist acts.

An act of terrorism is defined as a violent act or acts dangerous to human life, property or infrastructure committed by or on behalf of a foreign interest. Damage must occur in the United States or to U.S. air carriers or vessels. The loss resulting from any one terrorism event must exceed $5 million to trigger the protection afforded by the act; events committed during the course of war declared by the United States (except for workers' compensation) will not be considered terrorist acts under this legislation. The act established the following key elements:

Insurance companies providing commercial property and casualty insurance must participate in the federal backstop program and make insurance available for terrorism losses.

Participating insurance companies also must do the following according to the act:

According to the act, the deductible participating insurance companies must pay is based on a percentage of an insurer's direct premiums from the previous calendar year. When covered losses for a year exceed a company's deductible, the federal government will reimburse 90 percent of claims paid above the deductible up to an annual total loss of $100 billion for the insurance industry.

COMMENTS

Be the first to comment. Please log in to leave a comment.